One of the most frequent calls from homeowners to their agents is about the listing’s inactivity due to the lack of showings. The homeowner commonly believes that the home is shown only when a buyer walks through the house with an agent.

One of the most frequent calls from homeowners to their agents is about the listing’s inactivity due to the lack of showings. The homeowner commonly believes that the home is shown only when a buyer walks through the house with an agent.

Today’s buyers are more sophisticated than in the past due to the abundance of information available to the public on the Internet. There are seemingly inexhaustible sites with homes for sale, valuation estimates and virtual tours. There are extensive mapping sites with satellite images, traffic conditions, entertainment, shopping and other points of interest.

There are actually three legitimate types of property showings. A knowledgeable buyer can view a home for sale online and make a reasonable determination of whether the home will fit their needs. Occasionally, buyers will drive by a home to get a feel for the home and also the neighborhood which might cause them to eliminate any further examination or consideration.

The third type, the physical showing, certainly gives the buyer the opportunity for the closest scrutiny but is generally reserved for properties that have passed the inspections of at least one other type of showing.

Sellers should be aware of the different types of showings and that a sales agent’s job is to help the buyer find the right home. The listing agent’s job is to market the home so that the right buyer finds it either through their own efforts or that of the buyer’s agent.

You’ll need to earn $2.00 for every $1.00 you want to spend assuming you pay 50% of your earnings on income tax, social security and Medicare. On the other hand, you get to keep 100% of every dollar you save on your personal expenses because the taxes have already been paid.

You’ll need to earn $2.00 for every $1.00 you want to spend assuming you pay 50% of your earnings on income tax, social security and Medicare. On the other hand, you get to keep 100% of every dollar you save on your personal expenses because the taxes have already been paid. “I’d wish I’d know that before I made a decision.” If you’ve ever regrettably said this to yourself, having a checklist might have prevented the issue in the first place. This list of questions can provide you with things to discuss when interviewing a moving company.

“I’d wish I’d know that before I made a decision.” If you’ve ever regrettably said this to yourself, having a checklist might have prevented the issue in the first place. This list of questions can provide you with things to discuss when interviewing a moving company. The two most frequently quoted constants in life are death and taxes. Two more things would-be homeowners can expect in the near future are increases in mortgage rates and housing prices.

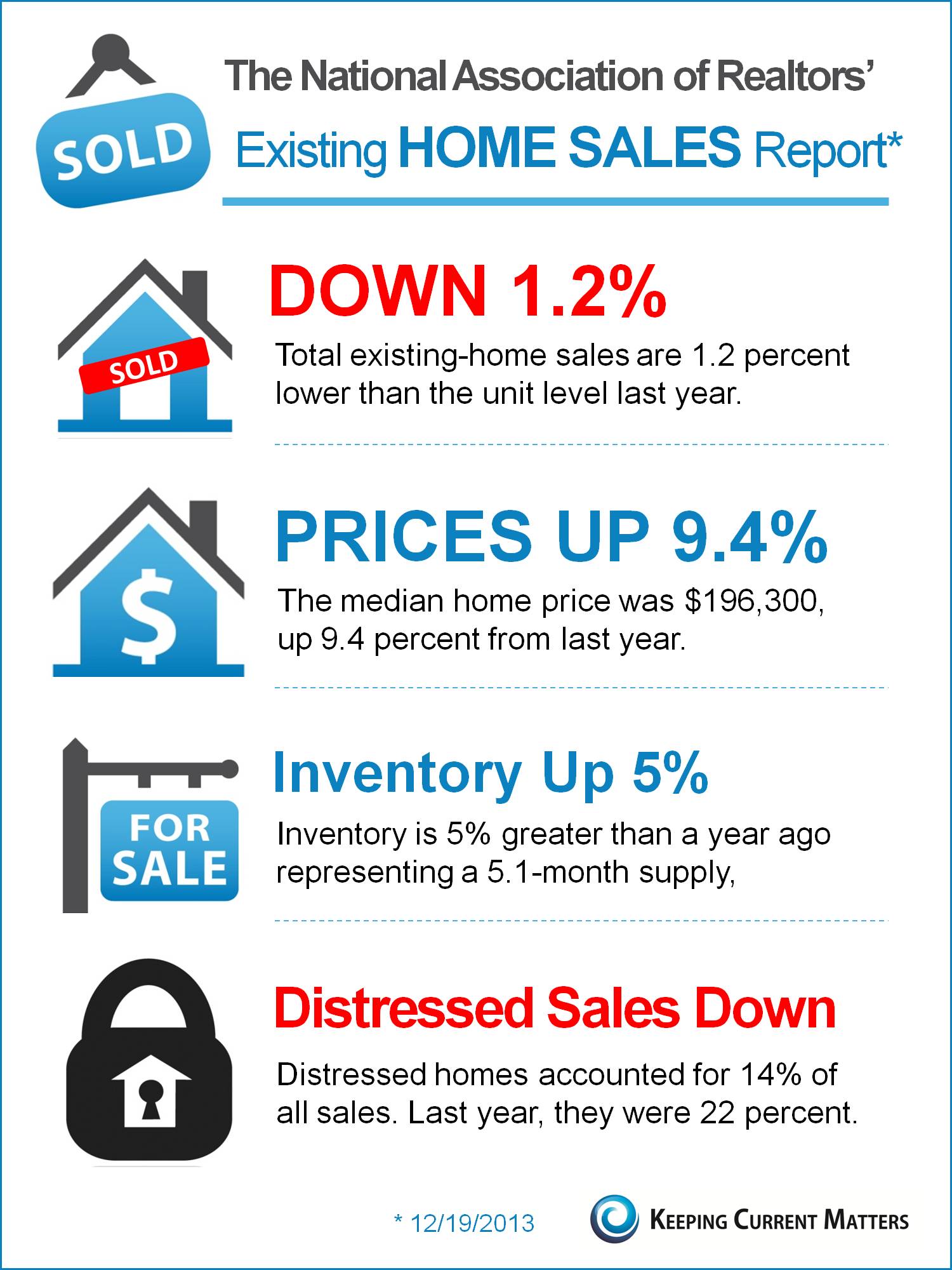

The two most frequently quoted constants in life are death and taxes. Two more things would-be homeowners can expect in the near future are increases in mortgage rates and housing prices.

{kind=link}